First off, apologies for not writing for a few weeks. I have had a few “too many irons in the fire” lately, and although still in that situation, I decided to take a break tonight and get a post out. And quite frankly, I am irritated at my government right now.

Our great, all-wonderful Federal Reserve (hint–sarcasm alert!) has decided to flood the corporate debt markets for the first time ever, and quite likely against their Congressional mandate and therefore illegal, to buy corporate debt securities. And this includes some bonds that are in the first tier of “High Yield,” or more commonly called JUNK, to support our large corporations. Yes, these same corporations who have lived off the benefit of too-low interest rates for the past 8-9 years. If you doubt this, look at the amount of refinancing activity since we were hit by the coronavirus, totaling $1.9 trillion. The dollar floodgates have opened up!

But my bone to pick this week is not with the Fed or the large companies, who are just taking advantage of the opportunity given to them. If I were a CFO of one of these companies, you’re darn right I would be issuing some corporate bonds as well. I do know a good deal when I see one!

However, lost in all of this noise is the lack of funding for our country’s small- and medium-sized businesses. Just in the past week, I have read a few articles about how we are leaving the small businesses at the curb as we make sure the large companies have a lifeline of financing to survive these tough times. Even Fed Grand Pubah Powell referred to small businesses as a “jobs machine.” And yes, we had the first round of PPP loans that were “targeted” to small businesses. Yes, those with less than 500 employees. Really, 500? When did that constitute “small” businesses? And there were many stories early on of large companies lining up at the small business trough, where luckily many of them were shamed into returning the funds.

But there were also other problems with these funds. For example, they were only for amounts to cover wages, and converted to a grant (not owed back) if you kept your employees hired during the pandemic. After these details were discovered, many companies who needed the money gave it back. Why? Because first, wages for many small businesses do not even start to cover fixed costs. Costs like rent, some amount of utilities, interest on existing loans, etc. Wages are one cost that is variable, where worst case you can temporarily lay off workers until you can reopen your business. Oh, and many workers that would have been laid off could actually make more money by getting unemployment, which made the whole premise of these PPP loans unnecessary.

Then, the PPP loan fund quickly ran out of funds. So many businesses who could have taken advantage were not quick enough to get in line. Now, I am beginning to read stories about how many of these small businesses are shutting for good. And quite frankly, our government assistance on this has been underwhelming.

I have purposely stayed out of “politics” on my blog, as I see no reason to alienate anyone. However, how is this for a neutral take on our representatives in Washington? I doubt there are any elected officials in Washington who care for our country as much as they care about being elected. I guess I have gotten a lot more cynical as I have gotten older. OK, that is all from me on politics.

So back to my small business rant. So late Tuesday night, as I did some light reading before falling asleep, I read the weekly Thoughts From the Frontline newsletter from John Mauldin (it’s free by the way, and a weekly must-read). And John had written about some alarming discoveries about the availability of financing for these struggling small businesses:

Stiff Drink Time

Whether it’s a bond or a bank loan, recovery potential is part of credit analysis. Defaults usually aren’t a 100% loss. What can we expect to get back if the borrower can’t repay? If you have collateral worth, say, 70% of the loan value, then you are taking less risk as the lender and can loan more freely.

Even better is to have the federal government standing behind a portion of the loan. That’s how Small Business Administration loans work. The SBA typically guarantees 50% to 85% of a loan amount, which lets banks offer more flexible terms than many small business owners could get on their own.

Keep in mind, many small businesses are struggling now but not all. Some have new opportunities in this environment. With capital, they could expand and maybe create jobs for the millions who need them. But they need capital first.

Last week I read and reposted a Twitter thread by someone describing himself as a consultant who helps franchisees get loans, often via SBA guarantees. I asked him to contact me and was able to verify his identity, though I can’t reveal it here. He described a terribly frustrating credit environment in his space. Below is a portion of his thread.

“The banks I work with are SBA, conventional lenders who service smaller loans under 2mm and generally smaller operators of these franchise systems, and then larger banks who provide loans to larger operators from 2-50mm. I’m short–20+ banks across ALL spectrum of SME lending.”

“I fund 400-500mm in loans per year through these banks. In February we were on pace to fund well over 500mm and potentially 700mm–growing exponentially year over year.” STIFF DRINK TIME. “Since April 1st we have funded 5mm total through only 2 banks. Let’s dive in as to why.”

“SBA banks–they have lending limits to 5mm. Congress has authorized them to go to 10mm in the CARES Act but they have ignored it. This will become important later. They currently have guarantees from the govt at 80%–pretty good right? DOESNT MATTER THEY STILL WON’T LEND.”

“In fact, they are pushing the government to guarantee 90% of the loans (and likely on their way to 100%–see my prior posts on the de facto nationalization of the banking system). In short SBA has SHUT OFF BORROWERS waiting for more from Uncle Sam.”

“Current excuses ARE PLAYING BOTH SIDES (and this applies to all banking segments). A chain with increased sales since pandemic–no loan. ‘We want to wait to see if sales increases are sustainable.’ Doesn’t matter that sales are up. They may not be ‘sustainable.'”

“On the other side for businesses with sales down–‘well we just aren’t comfortable sales will rebound and we have concerns over COVID.’ So, sales up = no loan. Sales down or flat = no loan. Operator size IRRELEVANT. Are some banks lending? Yes. This is 75-80% of SBA banks.”

“They are also being EXTREMELY selective on industries they will do. If you are in an industry with ‘large public gatherings’ you better pray to Santa Claus for money.”

So, businesses with solid revenue still can’t get capital even when the government will guarantee 80% of the risk. Economic recovery will be very hard if this persists. All those loans not being made represent business activity that won’t happen, buildings not constructed, jobs not created.

It doesn’t mean the situation is hopeless. But it probably means we will be stumbling through this morass even longer.

John Mauldin, Thoughts From the Frontline, August 8, 2020

Update on the Economy

Sorry, enough ranting. It takes a lot to get me riled up, but when I do get riled up, watch out. Let’s hope our elected officials remember the little guys who are the backbone of our economy. Although I fear it will be after the election, if at all, before it happens. I do appreciate John’s optimism, though!

So, how is the economy? I am actually starting to see some encouraging signs, even with the COVID spike in the U.S. right now. Retail sales are showing signs of life, and jobless claims continue to drop. Are we out of the woods? Well, not really. At least not yet.

I continue to read speculation that we may be getting a false sense of security, especially with the government stimulus that continues to flow. The additional $600 in federal unemployment support has, in my opinion, been huge. As I mentioned earlier, many who are laid off have more disposable income than when they were working. Add to that the stimulus checks everyone received, and that has likely kept things better than the underlying reality.

I was talking to my sister earlier, and she recounted a conversation her husband had with a salesman at a car dealership. My brother-in-law was inquiring why there was a very limited selection of cars on the lot, and the salesman said that with the stimulus checks, they couldn’t keep cars on the lot as they were selling so quickly. He then added, “Just wait a couple of months, when we get a lot of repos.” How true!

I believe President Trump made a smart move with the executive order to re-approve the federal unemployment benefit, albeit at $400 instead of $600. Illegal? Probably. To get reelected? Of course. But smart, as he boxed the Democrats in from being able to call him on it, as they would likely suffer politically. Sorry, got into the political ditch again. Oh well.

But that does likely keep the economy limping along at least through the election. And maybe we can continue to build momentum between now and then. However, not all is rosy.

In an article earlier this week, ZeroHedge discussed the “biblical” wave of bankruptcies now arriving, something I have been tracking since early on in this recession.

There was a spike in bankruptcies during the week of June 13-20, in fact the highest weekly filings since May 2009. And most of us can probably remember back to that time. And those are just larger companies with over $50 million in liabilities. As we just covered, many smaller businesses have also closed for good. So we are not out of the woods of this recession yet. And mortgage lenders are also preparing for a significant wave of delinquencies as well. In fact, it is being reported now that getting financing for mortgages, especially the larger jumbo mortgages, is difficult. Banks are uncertain about how much loss exposure they have with existing loans, so they have become very conservative with lending more and potentially adding to their exposure.

U.S. – China Relations

As we move further into this Fourth Turning, we should all keep watch for geopolitical issues that start to escalate. And there is no bigger area of potential conflict than the U.S. and China.

There are three primary kinds of wars. Trade wars, currency wars, and shooting wars. And maybe we can add a fourth, political war. When it comes to the U.S. and China, we have had a trade war brewing for a couple of years now, along with some currency spats. Things are now escalating politically, with the U.S. closing the Chinese consulate in Houston, followed quickly by China closing the U.S. consulate in Chengdu. Add to that the Hong Kong issue, and this is one to watch.

I am not about to get into who is right or wrong on any of these, especially being married to someone who is from China. So I remain diplomatically neutral, if for no other motivation than to have a happy, harmonious home life! But I am concerned with the escalations taking place. This week, we had a cabinet-level U.S. representative visit Taiwan for the first time ever, followed by China war games to the north and south of that island, along with an apparent build-up of military assets across the straits from Taiwan. Then, the U.S. flies a group of stealth bombers to Diego Garcia in Asia, added to the already-present patrols of aircraft carrier battle groups in the area. One wrong move by either side, and we could end up with shots fired.

Let’s hope cooler heads prevail. But this is not the only area where tensions could erupt. Greece and Turkey are close to blows in the Mediterranean as well, as Turkey and Russia square off on opposite sides in Libya. It’s getting hard to keep up with the potential areas for significant conflict. As Neil Howe has said, not all Fourth Turnings end in a shooting war, but many do.

That’s all for me this week. Thanks for letting me rant. And get into politics a bit, although I will endeavor to avoid that minefield in the future. We have enough minefields in the world without me adding to it.

Pretty simple guys. Stocks always go up, and even when they don’t they do.

Dave Portnoy, aka Davey Day Trader Global

These days, if you need to be entertained and have a good laugh, all you need to do is get on Twitter and see Davey Day Trader go up against the stock market “experts” and observe the back-and-forth banter. For those of you unfamiliar with Davey, he is Dave Portnoy, the president of Barstool Sports, who in the past spent a lot of his time focused on sports gambling. With no sports to bet on the past few months, and with a new load of cash on hand with the sale of 36% of his business to Penn National Gaming, Davey took up day trading to get his daily gambling fix. If crude language doesn’t bother you, then Davey is a good place to go to get entertained, especially if you follow the stock market.

The biggest debate in the financial world today is the age old question of whether the stock market will keep going up, or will we have a repeat of the late February downturn that will ruin the portfolio of Davey Day Trader and his legion of followers. As you know, I follow the markets and the economy closely, and I would put my money on us being in a Bull Trap rather than the start of a new Bull Market.

Bull Market – A bull market is a financial market of a group of securities in which prices are rising or are expected to rise.

Bull Trap – A bull trap is a temporary reversal in an otherwise bear market that lures in long investors who then experience deeper losses.

Investopedia

The key argument that we are in the beginning of a new bull market is driven by the belief that the flood of liquidity coming from central banks is finding its way into the financial markets and will continue to drive increases in stock prices and valuations. And there is merit to this argument, as in recent years there is a strong correlation between central bank-driven liquidity and stock prices. Another argument for a bull market is driven by the belief that the economy will quickly recover from the pandemic-driven shutdown, i.e. experiencing a “V-shaped” recovery.

The key argument that we are in a bull trap is centered on the belief that, over time, stock prices will reflect the strength or weakness of the underlying business conditions, reflected in the increase or decrease in corporate profits. The pandemic has pushed the world economy into a deep recession, and so far the stock market has not taken the drop in GDP into account in stock valuations. Those of us who believe we are in a bull trap are convinced that the economic recovery will not be quick or easy. and will eventually be reflected in business valuations.

If you have read my previous posts, you will know that I fall into the “bull trap” camp. In today’s note I will lay out the reasons I believe there is a high probability that we will see declines that will approach or fall below the March lows. I firmly believe that, over time, the stock market will reflect the economic performance the individual companies included in each exchange, regardless of the Fed’s actions to keep the market bubble inflated. And there is a very low probability that businesses recover quickly from the economic shocks we have endured since the beginning of 2020.

We have just gone through what appears to be one of the worst economic disruptions in history. The more I read, the more difficult it is for me to wrap my head around how disruptive the past 4+ months have been. One of my favorite financial market experts is John Mauldin of Mauldin Economics. He was one of the first financial commentators I began reading when I started my journey to learn about the economy and markets 10 years ago. In my last blog post I referenced his June 26 newsletter titled A Recession Like No Other. He closed that newsletter with an “instant classic” Twitter post from his daughter Tiffani that sums up, with some levity, what we are going through:

There is a lot of truth in that short post. Not only have we been hit by a pandemic, shutdown of businesses, supply shock, demand shock, protests, riots, etc., etc., etc., but the entire world has been hit by most of these at the same time. This is the stuff that would have made a fantastic end-of-the-world fantasy novel. And I still see financial market experts at the big firms predicting that we will recover from this by the end of the year. To me, this is wishful thinking to the hundredth power. I just cannot see us recovering in less than 2-3 years. And that’s if things go really well.

Why do I think this? Well, as usual my beliefs are shaped by the experts that I follow that make the most logical sense. And over the years I have found some great sources of wisdom that help me figure out where we are likely headed. So let me cover a few of the most impactful writings I have uncovered the past few weeks.

Up first is a July 6 article from Doug Kass, founder and president of Seabreeze Partners Management, Inc., who was bullish back in early March but has changed his view as the market has moved back up near all-time highs.

In aggregate terms, COVID-19 will likely have a sustained impact on the domestic economy – in reduced production and profitability – for several years, and in some industries, forever

Doug Kass, July 6, 2020

Doug then lists his concerns with the economy that will eventually negatively impact the markets.

Important Industries Gutted: Several key labor-intensive industries – education, lodging, entertainment (Broadway events, concerts, movie theatres, sporting events), restaurant, travel, retail, nonresidential real estate, etc. – face an existential threat to their core. For these gutted industries, we face, at best, an 80% to 85% recovery in the years to come. It should be emphasized that in the case of some of these sectors, like retail, Covid-19 sped up what was already a secular decline.

A Negative Knock-On Effect: Tangential industries, like food and other services, that surround less utilized office, mail and other spaces will also get hit. They, too, face at best, an 80% recovery, in the years to come.

Widening Income and Wealth Inequality: The combined unemployment impact will run deepen and cause not only adverse economic ramifications but lead to intensified social imbalances.

A Battered Public Sector: With a lower revenues base, the Federal government and municipalities will be forced to cut services (and unemployment).

Rising Tax Rates and Redistribution: To fund this shortfall, effective tax rates will be steadily rising – exacerbating the disruption above and creating a less than virtuous cycle.

Weak Capital Spending: With a large output gap and higher debt loads ($2.5 trillion of debt has been tacked on to year-end 2019 total non-financial debt of $16 trillion), the outlook for business fixed investment growth appears unappealing over the next several years.

Higher Costs, Lower Profit Margins: The surviving companies in a post Covid-19 world face higher costs of doing business. (Remember Amazon’s $4 billion rise in virus-related costs in its latest reporting quarter?)

The Competitive Influence of Zombie Companies Exacerbates Lower Profitability: Corporations will face further pressure on profit margins from “zombie companies” that compete aggressively on cost and take longer to die because of low interest rates and weak loan covenants.

Small Businesses Gutted: The greatest brunt from the pandemic is faced by small businesses that historically account for the largest job creators.

The Specter of a Secular Erosion in Unemployment: Permanent job losses will be surprisingly large – that’s a consumption killer.

More Cautious Business Confidence and Spending: The surviving companies, ill prepared operationally and financially, in early 2020 for the disruptive impact of Covid-19, will be forced to maintain a “buffer” of additional capital (and cash) in the event of another unforeseen event or tragedy. In all likelihood, this will make for less ambitious capital spending and expansion plans relative to the past.

A Political Stasis: Political divisiveness and partisanship could intensify – dimming the probability of constructive, pro-growth fiscal policy, so necessary in a log growth economy.

Doug Kass, July 6, 2020

Doug wraps up the letter by stating, “These are not the ingredient for a Bull Market or for rising valuations. Rather, the above factors may be an ingredient to:

Increased market volatility.

Rising economic uncertainty and cautiousness in the C-suite.

An unsteady period of growth.

Lower price earnings ratios.

More social unrest.”

All of these challenges, and Doug’s outlook, fit nicely into The Fourth Turning narrative I have been writing about. Fourth Turnings are typically times of unprecedented events taking place that push us into one crisis after another. This is much bigger than just the financial markets, although we can study the markets to see the signs of upcoming events as we move through the Fourth Turning.

Bankruptcies are on the rise, with 13 U.S. companies filing in one week in late June, the first week so far this year with more than eight. The sectors with the most filings are, no surprise, the consumer and energy. The highest profile bankruptcy filing in the energy sector Is Chesapeake Energy, a company that pioneered the fracking process to extract natural gas. A Deloitte study found that around 1/3 of U.S. shale producers are technically insolvent with oil prices at $35 a barrel. Oil prices have now climbed just above $40 per barrel, but there is no guarantee they will stay at this level. So more bankruptcies are likely to follow in this sector in the coming weeks.

Other recent bankruptcies, since June 15, include the following companies: 24 Hour Fitness (closing more than 100 of its 400 gyms), Brooks Brothers (closing 51 of 250 stores), Chuck E. Cheese, Cirque de Soleil, GNC (will accelerate closure of 800-1,200 of its 7,300 locations),

And there are companies that, for now at least, are not at risk of filing bankruptcy, but are still downsizing their operations as they figure out ways to survive the economic downturn and challenges in dealing with the fallout from the pandemic. Macy’s has announced a significant number of corporate layoffs. Bed Bath & Beyond announced on Wednesday it would close roughly 200 stores, around 13% of their stores. Their revenue for the quarter ended May 30 dropped 49%. The only good news is most of their stores are now open.

Bankruptcies and Store Closures Lead to PERMANENT Job Losses

There seems to be a belief out there that almost all job losses are just temporary, and furloughed employees will be hired back as businesses reopen and the economy gets re-started. This assumption leads directly to the belief in the “V-shaped” recovery. Sorry, I just don’t see it playing out this way.

If our economy was as strong as some believed as we went into this crisis, then I could have hope that there would be a quick rebound. However, as I have pointed out previously, our economy has been struggling really since the Global Financial Crisis, due to the continued expansion in the amount of debt that has made our economy extremely sluggish. We were headed for a downturn in the market before anyone was discussing COVID-19, and all that was needed was a small trigger to push us into a recession. Instead of a small trigger, we got a bazooka.

Walgreens Boots Alliance announced on Thursday it plans to eliminate about 4,000 jobs in the U.K., after announcing a quarterly loss of $1.71 billion, compared to a profit last year of $1.03 billion. Sales versus last year were flat, but the company estimated the pandemic cost them $700 to & $750 million in lost sales. And this is a retailer that was able to keep most units open during the past few months.

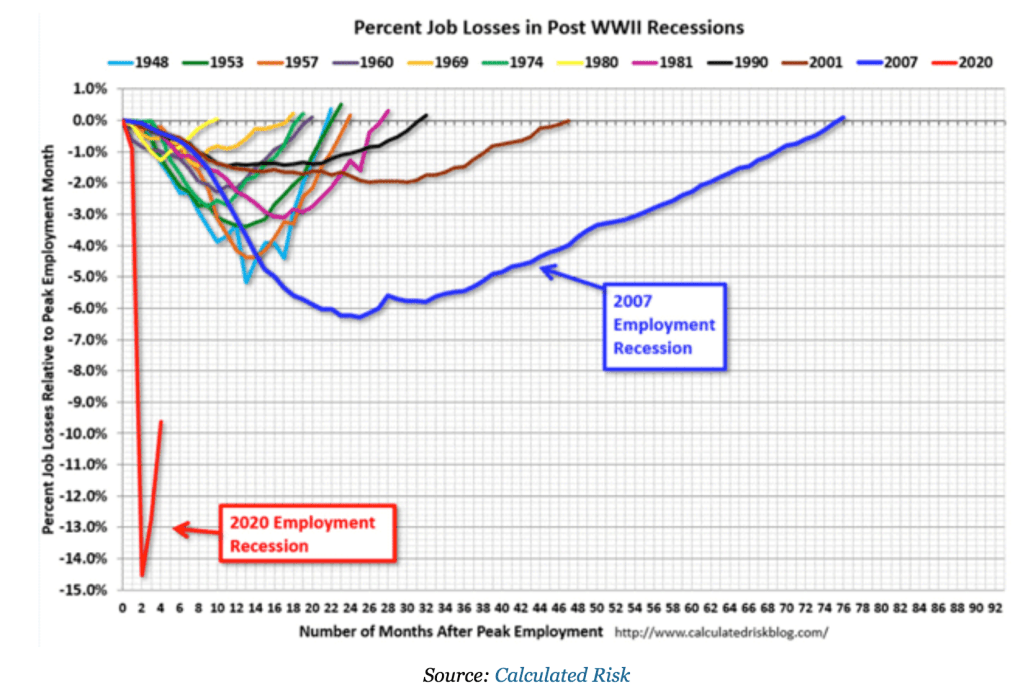

The graph above is from John Mauldin’s latest weekly newsletter, Stumble-Through Jobs Market. This graph really helps to give some perspective to the magnitude of job losses in the U.S. since the pandemic hit. Yes, there are a lot of job losses that are temporary this time, certainly more than in past recessions. However, even if a majority are temporary, we will still have a significant number of permanent job losses. Also, check out 2007, previously the highest number of job losses in a recession since World War II. It took around 6 years from the beginning of the recession before employment recovered to the same level, and close to 4 years from the peak unemployment level. Here is John’s take on the graph above:

…You can see in the 2007 line how long it took employment to recover after the last recession. At that pace, all the jobs will be back sometime in 2026 (Not a typo.) To assume the “V” seen above will continue in the same direction means thinking there will be a quick return to normalcy.

And maybe this time is different since at least some of the layoffs were temporary. The BLS data tries to distinguish between temporary and permanent job losses. That’s a moving target because employers don’t always know. They furlough people with the intent of bringing them back, but then find conditions don’t allow it. At some point, temporary job losses can turn into permanent ones…

This time around, we have seen the same percentage of permanent job losses in 4 months that took nine months in 2007, and over a year in the 2001 recession. There is every reason to think it will get worse before getting better. And it will get better…but probably not soon.

John Mauldin, Stumble-Through Jobs Market, July 11, 2020

I came across another article on June 26 discussing the unemployment claims and the prospects for a quick recovery:

Economists said the sluggish improvements dim prospects for a quick recovery. Further, a recent increase in coronavirus cases could affect efforts to reopen the economy–and get people back to work and spending money.

“We’re seeing a slowdown in layoffs, but hiring hasn’t picked up a tremendous amount,” said Nick Bunker, economist at the job site Indeed. “The recovery from this is going to potentially be a very long slog if we can’t get the virus under control quickly.”

…Macy’s Inc. is laying off about 3,900 corporate staffers as the retailer confronts a slow recovery.

“New Jobless Claims Hold at High Level, Signaling Long Slog,” Sarah Chaney, Wall Street Journal, June 26, 2020.

Earnings season for the second quarter kicks off this week, so we have only seen a trickle of earnings releases so far. So in the next 6-8 weeks we will learn much more about the true business impact of the pandemic shutdown and get a read on whether companies are seeing a significant improvement now that businesses and the economy are starting to open up. I plan to follow these releases closely to see if my pessimistic view is accurate or not.

The Bubble/Warning

One of my favorite reads is Sven Henrich, aka the Northman Trader. For anyone who has an interest in financial markets, I highly recommend you check out his website, http://www.northmantrader.com. He usually publishes a free article once every week or two, and he also posts a free video most weekends. His note on July, 6, called The Bubble, was a great note. In it he described how the Fed has created another market bubble with their recent actions to introduce massive liquidity into the economy.

At this stage markets are basically just a liquidity meth lab, an artificial behemoth constructed and subsidized by the Fed stepping in on any downside in markets. Following $3 trillion in liquidity injections in 3 months ($12 million annualized) markets have entirely disconnected from the economy and any traditional valuation metrics. The Fed’s role in managing markets is becoming ever larger and has now expanded into buying $AAPL [Apple] and $VZ [Verizon] bonds among others in addition to monetizing US debt. Call it what you like, just don’t call it capitalism, rather a nationalization of sorts.

The Bubble, Sven Henrich, July 6, 2020

That was the opening paragraph of the article. Wow, talk about hitting the nail on the head. Make no mistake, it is the Fed driving the stock and bond markets now, and nothing else. It is no secret. There is no one who denies this is the case. Unfortunately, this creates huge distortions in the market where economic fundamentals no longer matter.

Wall Street analysts have largely been made obsolete as earnings growth metrics have long been rendered irrelevant with everybody bowing to the Fed put as the primary reason for buying stocks.

Cases in point: The 2019 rally didn’t kick off until the Fed expanded its balance sheet via repo beginning in September 2019 and markets rallied 30% on zero earnings growth. The 2020 crash didn’t stop until the Fed went into QE unlimited mode, and the current rally stopped on June 8th for the broader market during the same week the Fed’s balance sheet peaked. Negative earnings growth for 2020 yet $SPX [S&P 500] is now flat on the year. Nothing happened. Nothing matters.

With no earnings growth during both years it is folly to pretend markets are about anything else but the Fed.

The state of affairs: The unemployed and poor are dependent on government handouts, the middle class is sweating staring at permanent job losses mounting as the top 1% and billionaire stock owner class is subsidized by the Fed as stocks keeps rising despite the worst economic backdrop in decades. All the while the Fed is steadfastly denying against all evidence that it is contributing to ever expanding wealth inequality even though that is precisely what it is doing.

The Bubble, Sven Henrich, July 6, 2020

Isn’t it reassuring that the 1% are being taken care of with the inflated stock market while the rest of us do our best to survive the current economic chaos. I cannot even watch Jerome Powell testify in front of Congress and deny that Fed policy is THE cause of wealth inequality in the U.S. Sven next covers the real drivers of the market rebound since March has all been due to the large tech stocks that are absolutely killing it, while all of the non-tech sectors are barely treading water.

But tech is increasingly dangerous and the bifurcation in market performances getting ever more apparent, a point I highlighted this morning on CNBC.

In equal weight there is truth I mentioned, highlighting the great distortion in markets. On equal weight basis the S&P 500 is actually sitting a the December 2018 lows when $SPX was trading at 2350.

The disconnect of course is driven by the Nasdaq which now has 7 stocks equaling $6.75 trillion in market cap hiding that most indices are in substantially worse shape than is advertised.

The message: The real economy is in much worse shape and the presumed “V” is not confirmed by the bond market or the banks. In fact the contrast in performance between the banking index and the tech sectors couldn’t be more crass…

Which brings me to tech itself. Overvalued and over owned. Massive valuation expansion over the past year.

The Bubble, Sven Henrich, July 6, 2020

Sven followed that note up with one this week titled Warning, where he discusses the warning signs he sees in the bubbly markets.

I know, we live in the age where trillions are tossed around like candy by central banks and governments and everybody’s eyes just glaze over as the numbers defy context and comprehension.

But let me throw a bit of reality into the mix and it’s absolutely mind boggling.

5 stocks have just added over half a trillion in market cap in just 6 days. Six days. Ponder that.

And they’re even higher on the open today.

5 stocks now have a combined market cap over $6.5 trillion. These very same stocks have added over $1.6 trillion in market cap in 2020. That would be a feat during any bull market during times of great growth, but in a historical recession?

So some of these stocks grabbed some market share during the shutdown, but don’t tell me $AAPL sold more phones during this.

It gets worse. Since 2019 these stocks have added over $3.2 trillion in market cap:

Now, if you can convince yourself to believe that these stocks have earnings growth stories to support market cap expansions anywhere near these figures I suppose you can convince yourself to believe anything.

During bubbles people will convince themselves of anything. And this is nothing new. After all people convinced themselves that tech’s valuations versus the rest of the economy were justified before. How did that work out?

Folks, we are witnessing the greatest market cap expansion in human history making the year 2000 look like child’s play. The combination of insane liquidity thrown at markets, the mechanics of automatic ETF allocations, retail and FOMO thirsty funds chasing these few stocks all look to contribute to the greatest market cap bubble in history.

Warning, Sven Henrich, July 9, 2020

Backing Sven’s view, I just read an article today about a CNBC interview with Mike Novogratz, billionaire investor and founder of Galaxy Digital, who had this to say about today’s markets:

We are in irrational exuberance – this is a bubble. The economy is grinding, slowing down, we’re lurching in and out of COVID, yet the tech market makes new highs every day. That’s a classic speculative bubble.

Interview with Mike Novogratz, CNBC (h/t ZeroHedge)

And ZeroHedge had this commentary on Mike’s interview:

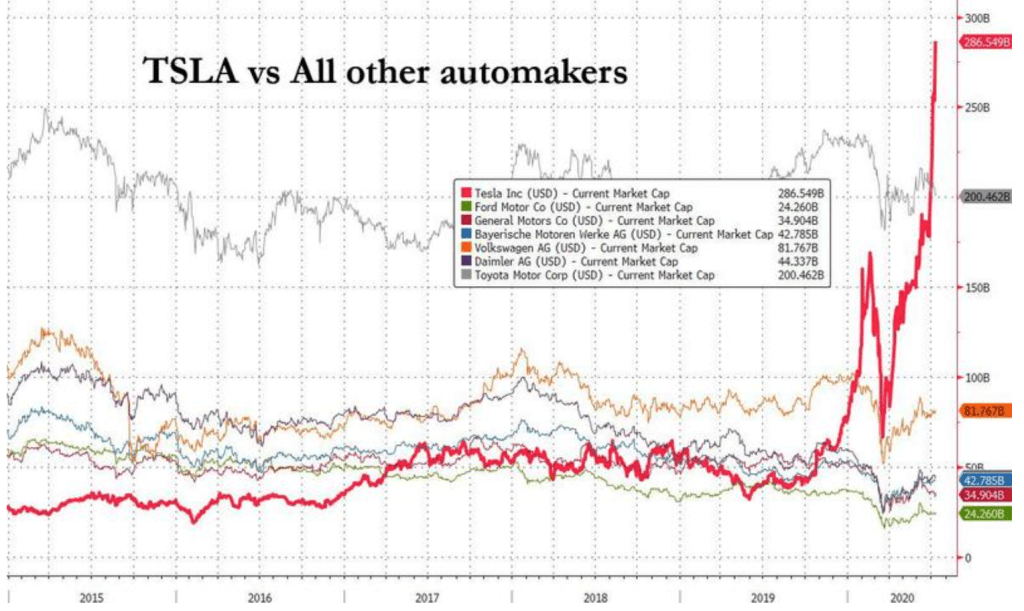

Echoing what BofA CIO Michael Hartnett said on Friday, when he cautioned that the disconnect between macro and markets has never been greater, which however is to be expected now that “government and corporate bonds have been fixed (“nationalized”) by central banks, so why would anyone expect markets to connect with macro, why should credit & stock price rationally,” Novogratz – like Stan Druckenmiller and David Tepper – has been sounding alarms about the stock market for months, yet the S&P 500 index has inched higher, erasing losses spurred by the coronavirus pandemic and notching its best quarter since 1998.

While so far Novogratz’ warnings have fallen on deaf ears, with Robinhooders clearly chasing momentum in such mega-bubble stocks as Tesla…whose market cap is now greater than that of Ford + GM +BMW + Daimler + Volkswagen combined…the man who made a killing buying bitcoin and ethereum ahead of the heard, said that the surge in equities, especiallly tech stocks, reminds him of the rally in Bitcoin prices in 2017, when the cryptocurrency went from $8,000 to almost $20,000 within a couple months due to retail interest…before crashing just as fast. It now trades at roughly half the price it reached during the December 2017 peak.

On June 24, the UCLA Anderson School of Management released its June quarterly UCLA Anderson Forecast on the outlook of the U.S. economy. This regularly scheduled release came after they revised their first quarter report for the first time in its 68-year history due to the shutdown of the economy as a result of the pandemic. And it sounds like the outlook for the U.S. economy just keeps getting worse.

Now, in its second quarterly forecast of 2020, the Forecast team states that the global health crisis has “morphed into a Depression-like crisis” and that it does not expect the national economy to return to its 2019 fourth-quarter peak until 2023

Press Release – UCLA Anderson Forecast, June 24, 2020

So let’s add this to the pile of evidence that the “V-shaped recover is just not going to happen. Their report had this to say about the U.S. economy:

“To call this a recession is a misnomer. We are forecasting a 42% annual rate of decline in real GDP for the current quarter, followed by a Nike swoosh’ recovery that won’t return the level of output to the prior fourth quarter of 2019 peak until early 2023,” writes the UCLA Anderson Forecast senior economist David Shulman in an essay titled “The Post-COVID Economy.”

“On a fourth-quarter-to-fourth-quarter basis, real GDP will decline by 8.6% in 2020 and then increase by 5.3% and 4.9% in 2021 and 2022, respectively,” he writes.

Shulman goes on to write that U.S. employment will not recover until “well past 2022” and that the unemployment rate, forecast to be about 10% in the fourth quarter of 2020, will still exceed 6% in the fourth quarter two years later. “For too many workers, the recession will linger on well past the official end date,” Shulman writes.

Shulman’s essay notes that the Federal Reserve acted with unusual alacrity by moving immediately to a near-zero interest rate policy and committing itself to supporting the corporate bond market, among other actions, and that the $1.8 trillion CARES Act moved quickly through Congress. He suggests that more relief will be needed this summer, and although a recovery is eventually forecast, it is expected to be moderate.

“Simply put, despite the Paycheck Protection Plan, too many small businesses will fail and millions of jobs in restaurants and personal service firms will disappear in the short run. We believe that even with the availability of a vaccine, it will take time for consumers to return to normal,” Shulman writes. He also states that the housing sector will be a lone bright spot in the recovery.

The forecast notes that while the economy seems to have hit bottom, it will take a while before GDP and employment levels reach fourth-quarter 2019 levels, as the huge debt buildup in both the public and private sectors dampen output. Looking beyond the forecast horizon of 2022, the pandemic has accelerated economic trends that were already moving toward increased digitization of business functions and online commerce.

“It has increased already-rising tensions with China and brought the E.U. closer together,” Shulman writes. “A major response to the pandemic has been the success of work-from-home, which looks like it will lead to long-term changes in the work and urban environments as workers avail themselves of more work/life options. In a nutshell, economic and housing activity will shift from large cities to mid-sized cities and away from the urban centers to the suburbs.

Press Release – UCLA Anderson Forecast, June 24, 2020

This article touches on an important point. As you start hearing about the economy recovering in the next few months, remember that this recovery’s starting point is at an extremely depressed level. Never has our global or national economy had an economic shock like we have just experienced. So if we see economic growth in the next few quarters around 5%, that sounds great, but remember we have likely just seen a 30%-40% decline in GDP. So it will take quite a few quarters of 5% growth to get back to where we were at the end of last year.

Conclusion: 2020 Versus 1929

So we have an economy in a severe, unprecedented recession (depression?), and a stock market, driven by a handful of tech stocks, sending the market back up near all-time highs. If you believe, as I do, that this market cannot remain this distorted long term, then the key question is when will it begin reflecting the conditions in the real world? That question is difficult to answer. There is a saying that the Fed can keep stock prices distorted longer than you can remain liquid, which is a warning about trying to time the big moves in the market. I learned long ago that it is a fools errand to try to exactly time market moves, but since I know where it is eventually headed, I can adjust my portfolio for the long term.

I finished reading a very good book about a month ago, Lords of Finance by Liaquat Ahamed. It follows the lives of the heads of the four key central banks (U.S., U.K., France and Germany) from the end of World War I through The Great Depression. This week, I went back and re-read Chapter 16, Into the Vortex, as I see a lot of similarities between today’s market and 1929, when that market bubble reached its peak. There are so many similarities between Davey Day Trader, and the “Robinhood” investors of today, and the numerous novice investors in 1929 who had that well-known Fear of Missing Out (FOMO) and invested in the market as it reached its peak.

The author starts the chapter with the following quote: “At particular times a great deal of stupid people have a great deal of stupid money…At intervals…the money of these people–the blind capital, as we call it, of the economy–is particularly large and craving; it seeks for someone to devour it, and there is a “plethora”; it finds someone, and there is “speculation”; it is devoured, and there is “panic.”–WALTER BAGEHOT

Let’s pull out a few excerpts from this chapter of the book, and see if you spot any similarities:

…while it was possible to predict the factors that caused any given stock to rise or fall, the overall market was driven by the ebb and flow of confidence, a force so intangible and elusive that it was not readily discernible to most people. There would be no better evidence of this than the stock market bubble of the late 1920s and the crash that would follow it.

The bubble began, like all such bubbles, with a conventional bull market, firmly rooted in economic reality and led by the growth of profits…

The first signs that other, more psychological, factors might be at play emerged in the middle of 1927 with the Fed easing after the Long Island meeting. The dynamic between market prices and earnings seemed to change. During the second half of the year, despite a weakening in profits, the Dow leaped from 150 to around 200, a rise of about 30 percent.

Lords of Finance

One big difference between past stock market bubbles and our current bubble is this one really didn’t start with a conventional bull market. Our current “bull” market has been driven by Fed liquidity, not economic reality. The big market distortions really started after the 2008 crisis, and growth since then has been very anemic.

It was in the early summer of 1928, with the Dow at around 200, that the market truly seemed to break free of its anchor to economic reality and began its flight into the outer reaches of make-believe…

That it was so obviously a bubble was apparent not simply from the fact that stock prices were now rising out of all proportion to the rise in corporate earnings–for while stock value were doubling, profits maintained their steady advance of 10 percent per year. The market displayed every classic symptom of mania: the progressive narrowing in the number of stocks going up, the nationwide fascination with the activities of Wall Street, the faddish invocations of a new era, the suspension of every conventional standard of financial rationality, and the rabble enlistment of an army of amateur and ill-informed speculators betting on the basis of rumors and tip sheets…

Trading stocks had become more than a national pastime–it had become a national obsession.

Lords of Finance

When I read “progressive narrowing in the number of stocks growing up,” I immediately remembered reading Sven’s article that discussed the big tech stocks, Microsoft, Amazon, Apple, Alphabet, and Facebook, being stocks that are driving this market higher. And what better way to describe Davey and the gang that a “rabble enlistment of an army of amateur and ill-informed speculators”? The similarities are almost scary! I am not sure I could describe todays environment as a national obsession, but it certainly is for a rather large segment of our population.

Anyone trying to throw doubt on the reality of this Promised Land found himself being attacked as if he had blasphemed about a religious faith or love of country.

As the crowd piling into the market grew, brokerage house offices more than doubled…These “board rooms” became substitutes for the bars shut down by Prohibition–the same swing doors, darkened windows, and smoke-filled rooms furnished with mahogany chairs and packed with all sorts of nondescript folk from every walk of life hanging around to follow the projected ticker tape flickering on the big screen at the front of the office.

Lords of Finance

So, an interesting parallel occurred to me when I read this today. In 1929, the brokerage houses became a substitute for the bars that had been closed due to Prohibition. And today, the stock market has become a substitute for sports gamblers who no longer have sports in which to bet on. I guess when our vices are taken away, we always find a replacement, but I had no idea how the stock market has taken the place of these vices on more than one occasion!

And you are attacked today if you criticize Davey and his crowd. Just ask Howard Marks.

The newspapers were full of articles about amateur investors who had made fortunes overnight.

The old crowd on Wall Street had a rule that a bull market was not in full stampede until it was being played by “bootblacks, household servants, and clerks.” By the spring of 1928, every type of person was opening a brokerage account–according to one contemporary account, “school teachers, seamstresses, barbers, machinists, necktie salesmen, gas fitters, motormen, family cooks, and lexicographers.” Bernard Baruch, the stock speculator who had settled down to a life of respectability as a presidential adviser, reminisced, “Taxi drivers told you what to buy. The shoeshine boy could give you a summary of the day’s financial news as he worked with rag and polish. An old beggar, hwo regularly patrolled the street in front of my office, now gave me tips–and I suppose spent the money, I and others gave him, in the market. My cook had a brokerage account.”

The stock pronouncements of shoeshine boys would become forever immortalized as the emblematic symbol of the excesses of that period. Most famously, Joseph Kennedy decided to sell completely out of the market when in July 1929, having already liquidated a large portion of his portfolio, he was accosted by a particularly enthusiastic shoeblack on a trip downtown to Wall Street, who insisted on feeding him some inside tips. “When the time comes that a shoeshine boy knows as much as I do about what is going on in the stock market,” concluded Kennedy, “it’s time for me to get out.”

Lords of Finance

And when an owner of a sports gambling website becomes the preeminent stock picker of 2020, maybe it’s time to move investments to the sideline and wait until the implosion clears.

The new folk heroes of the market were the pool operators, a band of professional speculators analogous to the hedge fund managers of today. They were typically outsiders, despised by the Wall Street establishment, who accumulated their fortunes–though they would soon enough lose them–by betting on stocks with their own and their friends’ money.

Lords of Finance

And the key phrase is “though they would soon enough lose them.” Market bubbles never end well. And unfortunately, it is typically those who are novices, trying for the first time to bet on the market, who lose out. I am hearing a lot that the market professionals are either sitting on the sidelines during the current market rally, or they are hedging their positions to protect their investments from a downside shock. And there is a reason they are doing this.

No doubt, with the Fed continuing to pump liquidity that finds its way into the markets, this rally could go on much longer than many believe possible. In many respects the stock market is driven by confidence, and right now most investors believe the Fed has their back and will provide support to the markets at any sign of a downturn. And so far they have been correct.

The challenge is understanding when you should get out. When does that confidence in the “Fed put” start waning? Who knows? But my strong advice is to trade carefully.

Greetings all, and happy Canada Day to all my Canadian friends, and an early happy Independence Day to my U.S. friends and family. Now that I have covered some background, let’s walk through the important developments in the past 1-2 weeks in regards to financial markets and the economy, which all tie in to our march further into the Fourth Turning

Financial Markets

What a roller coaster in the financial markets since late February. As the COVID-19 scare built, the financial markets took a big hit. Then, an incredible rebound occurred, starting in late March, pushing stocks back up close to, or in some cases, exceeding the all-time highs from February. Was this the shortest bear market in history? Not so fast. Beware of the potential for a classic “bull trap.”

The driver of the current stock market rebound has clearly been central bank policy and massive increased liquidity, led by our wonderful Federal Reserve Bank in the U.S. Before the COVID crisis hit, by almost any measure markets were overvalued. COVID was the pin prick that started the deflation of a financial asset bubble. However, central banks took quick action (much quicker and more aggressively than 2008), in effect re-inflating the market bubble. Their actions were quite breathtaking. It is no doubt that this has been the primary catalyst of the market rebound.

However, there is another phenomenon that is occurring that is pushing the U.S. stock market higher. Apparently driven by being stuck at home, bored, and nothing else to do, along with government stimulus checks and unemployment benefits (in fact, higher than some U.S. citizens take-home pay) providing some immediate cash with limited places to spend it, a new army of day traders have materialized, who have decided to “play” day trader to compensate for the lack of sports betting opportunities, led by DDTG (Davey Day Trader Global – https://twitter.com/stoolpresidente). In my opinion, this is classic market euphoria that has happened historically as markets are driven by extreme euphoria and FOMO (fear of missing out).

I read a lot in my spare time, and I recently finished a really good book, Lords of Finance by Liaquat Ahamed, that follows the story of the key central bankers who were the key financial leaders from World War I until the great depression hit. Our current day trading phenomenon reminded me of the market euphoria in the months leading up to the Great Depression. Back then, stock market investors were almost exclusively wealthy individuals. However, that changed in early 1929 as market euphoria took hold. The situation today seems very similar. And this time we have the Robinhood investing app and Davey Day Trader Global (DDTG) instead of the (quite tame in comparison) musings of Irving Fisher.

If you are not an intense sports fan, you may not know who DDTG (Dave Portnoy) is. He started a website that focuses on sports, betting, and other “bro” topics. And right before the pandemic hit, he sold 36% of his business, Barstool Sports, to Penn National, a casino company, for $163 million. Talk about great timing! And with no sports to talk about or gamble on, Mr. Portnoy decided to play the market with a portion of his windfall. In another stroke of luck, he started buying stocks right around the time that the market bottomed in March. With his mantra of “stocks only go up,” and being right SO FAR, he has proceeded to call out investing icons such as Warren Buffett (he’s “washed up…I’m a better stock picker than he is now”), Howard Marks and others. Of course, this is all to entertain his fans when there are no sports to discuss, but it does remind me of stories that were documented in the lead-up to the crash of 1929.

And many of DDTG’s followers are new investors, also sitting at home with no sports to bet on, that have signed up to use Robinhood to invest. Robinhood is a new online stock app where you can invest in the markets with no fee for buying or selling. It is the new hot app for the young crowd that have started investing for the first time. If you are one of these new investors, no offense, but you may want to study some Financial Markets 101 before you start investing your money. As proof of the absurdity of the markets, let’s revisit the Hertz bankruptcy that I covered a few weeks ago. As a reminder, Hertz filed bankruptcy on May 22. Let’s now look at the chart below from www.robintrack.net, a website that tracks Robinhood investor activity.

The green line is the number of Robinhood accounts that own Hertz stock, and the pink line is the share price. If you look at the far right of the graph, you will see activity leading up to and folllowing Hertz’s bankruptcy as our novice investors poured into the stock.

Date

# Robinhood Investors

Stock Price

February 20, 2020

1,064

$20.29

May 22, 2020

44,297

$2.84

May 25, 2020

44,354

$0.65

June 5, 2020

94,993

$5.53

June 15, 2020

170,814

$2.83

Robinhood users ownership of Hertz (HTZ)

As you can see, post-bankruptcy our new market participants drove the share price up from $0.65 at the time of bankruptcy to $5.53 almost two weeks later! That’s a 751% increase in the stock price! For a bankrupt company!!!! For new market participants, here is some advice: you may not want to invest your money in stocks where the company has filed bankruptcy. Why? When a company files bankruptcy, they have typically run out of cash and cannot get any further financing. Their liabilities are greater than their assets. The credit risk is so high, no one will lend to them. They may be able to restructure, sell assets, and continue to survive.

However, shareholders almost always get NOTHING! Zero. Nada. Zilch. They are the last in line to get anything of value in a bankruptcy. The holders of debt and other liabilities will get some compensation (usually much lower than what is owed), but not shareholders. If the company survives, it will typically issue new shares to new shareholders (in many cases a form of compensation to lenders), but existing shareholders prior to bankruptcy will never recover any of their investment. So our new breed of day traders must have assumed that since Hertz is a company with a very long history, it must be a great investment to get in at less than a dollar! Oops.

So the signs of market euphoria are everywhere. I am reading that the “smart money,” or professional investors, are sitting on the sidelines during this market rally. Why? Because the disconnect between the market and the underlying economy are at extreme levels, and as mentioned before, at historically high valuations. There is some small chance the market can stay elevated at these levels, driven by the massive liquidity provided by the Fed, but I believe it is much more likely that another drop will come soon, regardless of central bank actions that drive up markets.

One of my favorite reads is the bi-weekly newsletter Things that make you go hmmm by Grant Williams. In his most recent edition (June 21), titled Inconceivable, he covers some of the crazy things going on in the markets right now including Robinhood and DDTG.

Lord knows, in recent years, I’ve found myself uttering [Inconceivable!] on countless occasions but, since the beginning of this month, events have taken a turn for the preposterous…

Things that make you go hmmm, June 21, 2020

That was his introduction, and afterwards he covered the Hertz situation in detail as well as other similar situations. In reference to the new group of day traders, he comments as follows:

These people aren’t here for a long time, they’re here for a good time (although, lately, they’ve been having such a good time that, who knows? Maybe they’ll stick around a bit longer).

Things that make you go hmmm, June 21, 2020

We have certainly seen a bit of a pullback in the last week, which by no coincidence occurred at the same time as the Fed’s balance sheet started to contract a bit. I fully expect a lot of volatility for some period of time, with wild swings up and down. Trade carefully!

The Economy

The recession that we are now in is unlike previous recessions. Usually, recessions are triggered by an event in the financial markets, such as the dot com bubble in 2000 or the mortgage market collapse in 2007-2008, which then affects the economy. This time, it was the economy experiencing an extreme shock because of the virus hitting, causing businesses to shut down, resulting in a demand shock. This was after experiencing a supply shock when China, the world’s factory, shut down. It has created a chaotic situation for many businesses. The unemployment numbers are shocking, like nothing before with the speed in which it happened.

I read two different articles discussing this in the past few days (both are free newsletters). The first is Thoughts from the Frontline by John Mauldin, whose June 26 newsletter was titled “A Recession Like No Other.” Here are a few key points I gleaned from his analysis of the “Corona Recession,” with reference to recent published remarks from economist Woody Brock.

I thought we were headed for a credit crisis, centered on corporate debt rather than mortgages, as happened in 2008. The Fed’s decades-long easy money policies have many businesses leveraged to the hilt. That remains the case and could still become a bigger problem but for now, we are in something unique: a supply-and-demand-driven recession. Specifically, service supply dried up almost overnight as people lost those service jobs and, as will see, those with more money started to save dramatically more, further reducing demand.

Normally, some kind of trigger or “shock” makes business activity contract. Tighter credit or higher interest rates are often the culprit, not simply falling sales. Unable to finance continued operations, businesses close and lay off workers, who then reduce their consumption. The effects cascade through the economy and recession begins.

This time, the shock came with the coronavirus and our reaction to it. Note, it wasn’t just government-ordered shutdowns. Data now shows consumer spending started failing weeks before governors acted. Retail service businesses saw store traffic falling and, with risks to employees and customers rising, many closed even when not required to. But the result was the same: Business activity contracted and triggered a recession.

John Mauldin, Thoughts From the Frontline, June 26

I then read Bill Blain’s The Morning Porridge June 29 edition, titled “What if it’s just begun?”

This crisis is unlike anything I’ve experienced before. Normally a market crash is [an] explosive event – it occurs when something in the financial sphere breaks; like confidence in housing and financial systems in 2007, or valuations in the Dot.Com crash, or faith in credit constructs like during the European Sovereign Debt crisis in the 2010s. In each case of financial mayhem I’ve experienced since the Great Perp Crash of 1986, the initial shock and horror gradually lessens as the market discounts the shock, shrugs it off, and carries on…

This time it feels different. The crisis started off with a meteor strike – the virus. We’ve never seen anything impact the real economy so dramatically. Normally – it happens the other way around: financial crashes impact the markets and only then does the pain trickle down into the real world. This time it’s real jobs and production that got hit first. That’s fundamentally different.

I’m not convinced that markets really understand that difference. The effect on the real economy of financial failure is felt in terms of the flow of capital to businesses. If a bank blows up – it will impact savers and borrowers. This time we’re looking at how will crashing earnings and diminished rental incomes hit the financial markets – but they are behaving as if it’s just another round of QE [quantitative easing] Infinity for the markets to arbitrage. As we all know markets are completely delinked to the real world at present.

Yet, the damage the real world is going to inflict on financial markets is going to be huge – but that’s not what I see the banking regulators and authorities preparing for. They’re pushing financial institutions to participate by easing lending and supporting confidence. You can understand why – yet they also know a crisis [is] coming. Just read the dissenting statement by Fed Governor Lael Brainard after she stepped back from the Fed’s decision to allow bank dividends: “many large banks are likely to need greater loss absorbing capital to avoid breaching their buffers in adverse circumstances nest year.”

The bottom line is global central banks know a financial crisis is possible/probable.

Bill Blain, The Morning Porridge, June 29

So this time is really different, and not in a good way. Our central bankers, already incompetent in so many things, appear to be “flying blind” in our current situation. I fear we are beginning to see the last few snowflakes that will eventually start an avalanche of actions that will drive negative consequences for the economy. There are so many companies that have increased debt on their balance sheets, driven by cheap money. And in too many cases, they have used this cash to buy back stocks, increasing their executive bonuses at the expense of adding financial risk to their company. I do not see this ending well.

Bankruptcies continue to pile up. Chesapeake Energy, a company that pioneered fracking to extract natural gas, was the latest headline casualty. Also added to the list are Whiting Petroleum, Cirque de Soleil, Aeromexico and Chuck E. Cheese. We have now had 17 major retailers file for bankruptcy so far this year, including GNC, Roots USA, Tuesday Morning, True Religion, Centric Brands, Modell’s Sporting Goods, J.C. Penney, Art Van Furniture, Stage Stores, Bluestream Brands, Aldo, Pier 1, Neiman Marcus, SFP Franchiees Corp., and J Crew. Here in Canada where I now live, several well-known retailers have filed, including Reitman’s, Sail, and Aldo. I am confident the list will continue to grow. Many of these companies will survive, but with fewer stores and fewer employees. And this is on top of last year’s retail bankruptcies that resulted in over 9,500 stores closing. This year will be worse.

As far as who could be next, keep an eye on Michaels, Carter’s, Tailored Brands, Game Stop, Designer Brands International, Bed Bath & Beyond, and Ascena. There are also a lot of restaurants at risk, especially those that rely on the dine-in segment. And if a large number of retailers file for bankruptcy, who gets impacted? First in line, the owners of the shopping centers where these stores are located.

So next you should keep an eye on retail Real Estate Investment Trusts (REITs), especially those with a lot of debt. If tenants are not paying rent, and leases get discharged in bankruptcy resulting in vacant units, this will inevitably lead to the owners of that real estate having financial difficulties. The avalanche starts picking up steam. Travel-related industries are also being hit hard. The CEO of Air BNB even said this week that the travel industry will never get back to “normal,” referring to pre-COVID-19 conditions.

I ran across a good article about the impact on retail and shopping centers this week. There are so many small independent retailers and restaurants that will not make it through this crisis.

In short, bricks and mortar retail has been caught in a pincer movement, flanked on one side by Covid-19 itself, and on the other site by its cure. You know this already: The virus separated us, the cure institutionalized that separation, forcing societal shutdown that has driven us into our deepest recession in perhaps living memory, a recession that seems certain to run several years. The coronavirus means we will remain wary of one another until there’s a vaccine, perhaps longer; the cure means a majority of Americans will have little to spend.

What does this portend? Putting aside kids swarming the beach towns, few of us wish to take more risks than necessary. Driving on a freeway entails infinitesimal risk, but we do it to get somewhere; going shopping now involves a minute risk, but we accept it if the shopping is essential…

Our essential retailers – supermarkets, drug stores, banks, convenience stores and gas stations – are doing fine; in fact groceries and gas are killing it. Someone’s idea of essential, liquor stores and cigarette shops, are not complaining either…

Personal services – beauty shops, nail salons, dry cleaners, massage parlors, yoga studios and gyms, etc. – win on cheap, but lose on distancing. Fortunately for some – notably, hair and nails – essential trumps distancing; these shops will come back swiftly. Others, like dry-cleaning and massage, are less essential and will take time to regain their pre-Covid levels.

Finally, there’s the sweat subcategory: small gyms, bike spinning parlors, yoga studios, etc. Absent an amazing vaccine, these tenants may be in serious trouble. You can’t make money at 50 percent maximum capacity and you’ll never convince some meaningful percentage of your customers that they’ll be safe dodging sweat in a tightly packed room.

Following the distancing/cheap lodestone, food shapes up like this: drive-throughs are golden, traditional take-out (e.g. pizza) is rocking, and those restaurants that can successfully ramp up their take-out should be fine.

By the way, the coronavirus didn’t create retail’s larger problem – excess capacity – it merely pulled its curtain back. According to Forbes, we have roughly 50 square feet of retail space per capita in the USA while Europe has just 2.5 square feet. Washington DC has a restaurant for every 103 residents, while San Francisco has one for every 201 residents. That’s a lot of competition…

Bringing this home: To date, we’ve permanently lost half-dozen retailers, from restaurants to clothing to massage. Tenants who in effect said sue me, I’m taking a hike. To compound this unpleasantness, it would be fair to say that replacement shop tenants are just behind the spotted owls on the endangered species list. But if there is a safe harbor in retail, it’s a supermarket center in a good residential neighborhood. Without plan or compass, we happened to bob into that harbor years ago.

John E. McNellis, Principal at McNellis Partners, via Wolf Street (h/t ZeroHedge)

That is a great summary by a retail shopping center owner. Enclosed malls are the clear loser so far in this crisis, with open-air power centers and neighborhood centers anchored by a food retailer being best positioned to weather the storm. As difficult as the past three months have been for the retail and travel industries, another disruption with infections ramping up in the south and west in the U.S. is a problem. I believe there will be a collapse in these industries if a significant portion of the U.S. goes into a lockdown again. It will be brutal.

Shockingly, there are still economists that are predicting a quick “V-shaped” (i.e. rebound by year end) economic recovery. Seriously, what are they smoking? UCLA Anderson and senior economist David Shulman have updated their second quarterly economic forecast, with some interesting tidbits.

…the virus pandemic has ‘morphed into a Depression-like crisis’ with no V-shaped recovery until 2023.

‘To call this crisis a recession is a misnomer. We are forecasting a 42% annual rate of decline in real GDP for the current quarter, followed by a ‘Nike swoosh’ recovery that won’t return the level of output to the prior fourth quarter of 2019 peak until early 2023′ Shulman writes in a report titled “The Post-COVID Economy.”

“Simply put, depsite the Paycheck Protection Program, too many small businesses will fail and millions of jobs in restaurants and personal service firms will disappear in the short run. We believe that even with the availability of a vaccine, it will take time for consumers to return to normal” Shulman writes.

Zero Hedge, “;Depression-Like Crisis’ Unfolding With No V-Shaped Recover Until 2020, UCLA Anderson Warns”, June 25

That is not encouraging at all.

So, who holds the debt of these companies that are filing or are at risk of filing for bankruptcy? Banks, pension funds, sovereign wealth funds, insurance companies, etc. hold most of this debt. And with unemployment continuing to grow, and the extra federal subsidies for unemployed workers set to expire in a few weeks, it is difficult to see how consumer spending will get back to the levels before the coronavirus hit.

Chris Whalen of The Institutional Risk Analyst had some interesting insights on the commercial real estate environment.

So how big is the impending commercial real estate bust in the US? Bigger than the residential mortgage bust of the 2000s and also bigger than the commercial real estate wipeout of the 1990s, including the aftermath of the Texas oil boom of the late 1970s and 1980s…

The latest Mortgage Bankers Association survey shows that commercial banks continue to hold the largest share (39 percent) of commercial/multifamily mortgages of $1.4 trillion. Agency and GSE [Government Sponsored Enterprise] portfolios and MBS [Mortgage Backed Securities] are the second largest holders of commercial/multifamily mortgages, at $744 billion (20 percent of the total). Life insurance companies hold $561 billion (15 percent), and CMBS [Commercial Mortgage Backed Securities] and other ABS [Asset-Backed Securities] issues hold $504 billion (14 percent)…

The fact of the COVID19 lockdown, the riots and looting following the killing of George Floyd by the Minneapolis police, and the coincident rise of telecommuting, which keeps people away from the large metros, raises questions about the entire economic structure of cities. So long as social distancing is required or even the preferred option, many of the institutions and structures within the big cities no longer function.

Connor Dougherty and Peter Eavis reported in the New York times on Friday: “Faced with plunging sales that have already led to tens of millions of layoffs, companies are trying to renegotiate their office and retail leases – and in some cases refusing to pay – in hopes of lowering their overhead and surviving the worst economic downturn since the Great Depression. This has given rise to fierce negotiations with building owners, who are trying to hold the line on rents for fear that rising vacancies and falling revenues could threaten their own survival…”

So how big will the commercial real estate bust be in 2020-21 and beyond? In 1991, the FDIC reports, “the proportion of commercial real estate loans that were nonperforming or foreclosed stood at 8.2 percent, and the following year net charge-offs for commercial real estate loans peaked at 2.1 percent.”

In 1991, the net charge off rate for all $1.6 trillion in bank owned real estate loans was less than 0.5%. Multifamily mortgage loans peaked in Q4 of 1991 around 1.5% of net charge offs but remained elevated until 1996.

But this time is different. Based on our informal survey of REIT valuations and individual assets, we think that the world has been turned upside down for many investors. Actual LTVs [Loan-to-value ratios] for urban commercial and luxury residential assets in many metros are well-over 100 and are likely to be restructured, albeit over a period of years. As we noted last week, it’s all about buying time.

We think that net charge offs on commercial loans could rise to 2-3x the peaks of the 1990s, with loss rates at 100% or more in some cases, and remain elevated for years to come as the workout process proceeds.

Failing some miraculous economic rebound in the major metros, look for credit costs related to commercial real estate climb for REITs, CMBS investors, the GSEs, and banks in that order of severity. Figure a 10% loss spread across $5 trillion of AUM [Assets Under Management] over five years?

Chris Whalen, The Institutional Risk Analyst, H/T ZeroHedge, June 8

If I can summarize, a “V-shaped” recovery is pipe dream. The dominoes are already starting to fall. Many of the job losses to date will likely move from temporary to permanent. Our economy is no longer driven by manufacturing, as it today is primarily a service economy. And when many service industries, such as retail, restaurants, and travel, have suffered the brunt of COVID-19, a significant portion of our economy is suffering.

Conclusion

I originally planned to also cover some geopolitical events in this post, but my ramblings on the financial markets and the economy were quite a bit longer than I anticipated. So I will cover some geopolitical events from the past few weeks in my next posting (hopefully this weekend).

Our economy has taken a gut-punch, and we are staggering. Unfortunately, I do not believe the Fed’s actions are the cure for what ails us. As I covered above, this shock to our economy and financial markets is unique. And our ability to recover from this is negatively impacted by the central bank’s actions over the past 20-30 years to “kick the can down the road.” At some point, we will reach the end of the road, with nowhere to go other than off the cliff that is dead-ahead.

We find ourselves in the midst of our Fourth Turning crisis, with no easy way out. The next few years will be hard, very hard. But I still believe in American Exceptionalism. We will come out of this stronger than before. We have no choice but to “hunker down’ and face the challenges full-steam ahead. But the silent majority in our country must stop the silence, and be heard. Otherwise, we will lose all those attributes that have made us exceptional. And we need true leadership! I have yet to see any real leaders in our government step up to give me confidence that we have leadership in our country that can maneuver us through this crisis. We are not a country of chaos and disunity. Although if you viewed the current events of the past few months, it doesn’t seem to be the case.

I have spent the majority of my career in the real estate industry, and I find myself in the middle of the current economic storm. I am just very thankful that I am employed by a company that has taken a conservative financial approach to managing their business, with a strong balance sheet that can survive when others become insolvent. I am also very thankful that I have a job where I can effectively work remotely from home. I know many others who do not have that option.

Let’s prepare ourselves for the challenges ahead. I hate to say it, but I doubt we will ever go back to the good times we had just a few short months ago. I have heard many speak of the “new normal,” and I think that is absolutely correct. Change is hard. And we all now face a multitude of changes in our life. Economic. Social. Geopolitical. One of my favorite quotes, from a Kellly Clarkson song, is, “What doesn’t kill you makes you stronger.” Let’s all persevere, and come out stronger on the other side of this Fourth Turning. If you have no idea what I am talking about when I reference the Fourth Turning, go check out my post on the subject. Check out The Fourth Turning website (https://www.fourthturning.com/). And read the book. I know some of you have already done that.

Happy Canada Day and Independence Day (and Happy Summer to all others),

This week I am going to build on my last post of a couple of weeks ago and cover the central bank mis-steps in more recent times that are now putting the world at risk of significant economic shocks. Although the timing is difficult to predict, I expect the 2020s will be an extremely challenging decade, politically, socially, and economically. For more on why I believe we are on the cusp of these challenges, please read my previous post The Fourth Turning.

So first let’s recap a few key points from Part 1, as follows:

The mis-steps began with the added mandate given to The Fed in 1978 to maintain full employment.

This mandate is contradictory to the Fed’s primary mandate of maintaining price stability for a free-market, capitalist economy, as the process of “creative destruction” in a free market leads to business failures and temporary job losses.

This has led to unprecedented sizes of central bank balance sheets across the world and increasing debt loads for many governments. Corporations and individuals are also maintaining high debt levels.

One key point I failed to cover in the last post is a key reason why it is now possible for governments to introduce unlimited amounts of money into circulation today. In 1971, President Richard Nixon made the decision to “temporarily” take the United States off the gold standard. Under the gold standard, all U.S. currency was convertible into gold. This acted as a control mechanism to limit the amount of currency that could be put into circulation, as there had to be enough gold in the vaults at the Federal Reserve Bank of New York and Fort Knox to support this convertibility. Oh, and 49 years later that “temporary” move off the gold standard has never been reversed.

Nothing lasts longer than a temporary government program.

President Ronald Reagan

I also want to expand a bit on the mandate on full employment. Yes, I know this sounds like a good thing. It is tough when people lose their jobs. But a key foundation of capitalism is a “survival of the fittest” environment where the strongest, most well-run businesses survive while weaker companies go away. This puts pressure on these businesses to continuously innovate and improve, and this is the environment that has created the strongest economy the world has ever seen. And the strides the world has made since the beginning of the industrial revolution is nothing short of miraculous. So capitalism has proven to be the best economic system for maintaining strong businesses, maintaining high productivity, and allowing standards of living to grow and citizens to thrive. It is not a perfect system, but so far it is the best that we as a civilization have devised.